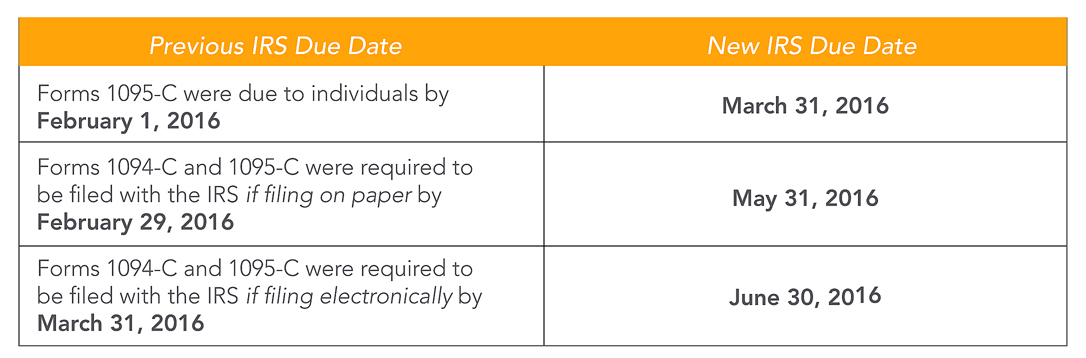

Specifically, the Notice extends the deadline for furnishing to individuals the 2015 Form1095-C,Employer-Provided Health Insurance Offer and Coverage, and for filing with the IRS Forms 1095-C and corresponding 2015 Form 1094-C,Transmittal of Employer-Provided Health Insurance Offer and Coverage Information Returns, as follows:

The IRS likewise extended the due dates for the 2015 “B” Forms, the Form 1095-B,Health Coveragefrom February 1, 2016 to March 31, 2016, and the Form 1094-B,Transmittal of Health Coverage Information Returns, from February 29, 2016 to May 31, 2016, if not filing electronically, and from March 31, 2016 to June 1, 2016, if filing electronically.

These extensions apply automatically to all filers. Applicable large employers, health insurers, employers that sponsor self-insured health plans, and other providers of minimum essential coverage do not need to submit or do anything to take advantage of the new due dates. Filers who already submitted an extension request will not receive a reply from the IRS nor are they eligible for additional time extensions to the extended due dates announced in the Notice. Also, keep in mind that these extensions apply only to 2015 returns and information statements and do not apply in future years (e.g., the 2016 Form 1095-C must be furnished to individuals on or before January 31, 2017).

The Notice also notes that employers or other coverage providers that do not comply with the new extended due dates will remain subject to penalties under Code Sections 6722 or 6721 for failing to timely furnish and file, but encourages employers and other coverage providers that do not meet the extended due dates to nonetheless furnish and file, because the IRS will take such furnishing and filing into consideration when determining whether to abate penalties for reasonable cause. When deciding on penalties, the IRS will also take into account whether an employer or other coverage provider made reasonable efforts to prepare for reporting the required information and furnishing it to employees and other covered individuals, such as gathering and transmitting the necessary data to an agent to prepare the data for submission, or testing its ability to transmit information to the IRS. In addition, the IRS will take into account the extent to which the employer or another coverage provider is taking steps to ensure that it is able to comply with the reporting requirements for 2016.

The Notice provides that the IRS “is prepared to accept filings of the information returns on Forms 1094-B, 1095-B, 1094-C, and 1095-C beginning in January 2016,” and encourages employers and other coverage providers to furnish statements and file the information returns “as soon as they are ready.”

The Notice also provides guidance and relief to individuals who might not receive a Form 1095-B or Form 1095-C by the time they file their 2015 tax returns. For more details on this extension and what it could mean for you, join us for an ACA Special Edition Webcast:

Understanding the Impact of the IRS ACA Annual Reporting Extensionon January 12, 2016. Check

hereto register.

ADP Compliance Resources

ADP maintains a staff of dedicated professionals who carefully monitor federal and state legislative and regulatory measures affecting employment-related human resource, payroll, tax and benefits administration, and help ensure that ADP systems are updated as relevant laws evolve. For the latest on how federal and state tax law changes may impact your business, visit the ADP

Eye on WashingtonWeb page located at

www.adp.com/regulatorynews.

ADP is committed to assisting businesses with increased compliance requirements resulting from rapidly evolving legislation. Our goal is to help minimize your administrative burden across the entire spectrum of employment-related payroll, tax, HR and benefits, so that you can focus on running your business. This information is provided as a courtesy to assist in your understanding of the impact of certain regulatory requirements and should not be construed as tax or legal advice. Such information is by nature subject to revision and may not be the most current information available. ADP encourages readers to consult with appropriate legal and/or tax advisors. Please be advised that calls to and from ADP may be monitored or recorded.